Throughout time, the single greatest creator of wealth in human history has been global trade, and market friction has been the greatest inhibitor to create wealth. Over the years, as businesses and processes have evolved and become more automated, the industry has overcome many different sources of friction.

The emergence of tools, institutions and rules of trust have mitigated potential business transactions risks, as well as technology innovations helped companies to eliminate their inefficiencies, although many business transactions remain inefficient, expensive and vulnerable until today. That’s where Blockchain comes to the life. This innovative technology, which creates a permanent, safe and transparent record of transactions, brings an incredible potential to obviate intractable inhibitors across many, if not all, industries.

Read: Understanding BYOD in the Pakistani Business Context

Further to that, Blockchain offers a decentralized register of ownership by recording every single transaction in the system, from creation of a block and through any number of transfers made. Every computer tapped into the system stores a copy of this Blockchain, and before a transaction can be made the system checks that their version of the Blockchain is in sync with all other versions within the network. What that means is that by using Blockchain technology, all users know who owns every block, at any time.

In the current digital economy, the potential uses for such a powerful decentralized register goes beyond use only in digital currencies, which is the heart of the Blockchain creation. There is a potential to revolutionize the security of ownership for an enormous range of high value transactions throughout many different industries and markets.

Read: 5G Wireless Behind AT&T, Verizon’s Big Buys

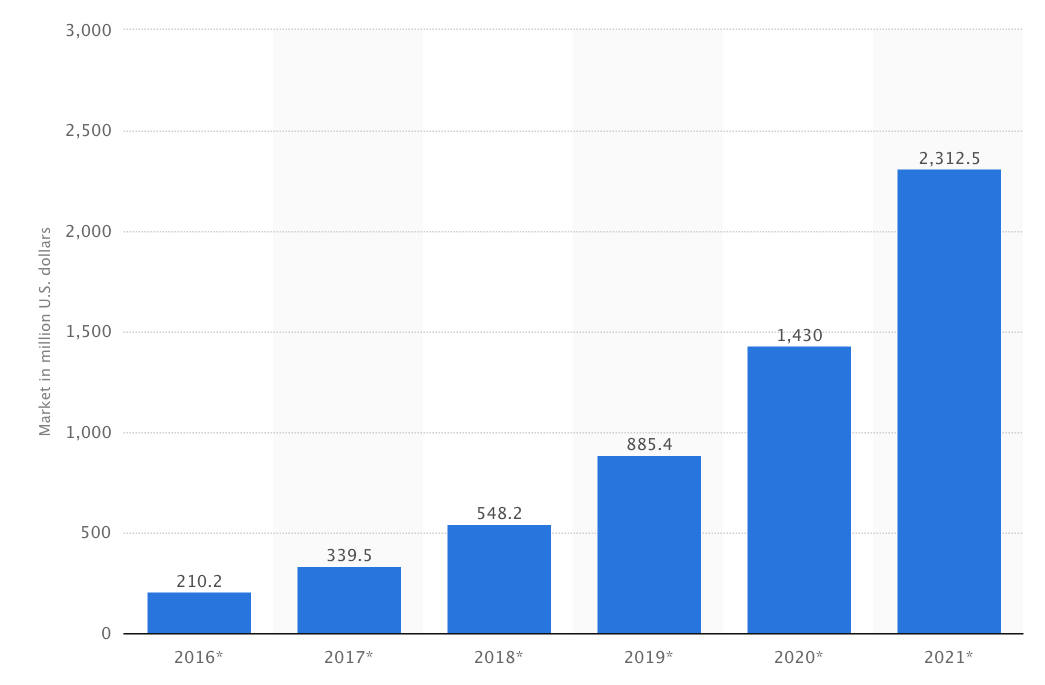

Meanwhile, blockchain has attracted intense interest from the investment community and some major corporations. Venture capitalists have poured a huge amount of investment in startups and companies investing in this new technology. The Blockchain market is expected to reach more than 2.3 billion dollars in 2021, which represents a 10-times growth from the size of this market in 2016, as shown on the chart below:

The question that many CIOs, IT leaders and CEOs still ask is how does Blockchain work? The Blockchain technology is basically a distributed database, just like, to put on perspective, an enormous global spreadsheet that runs on millions of different computers, with no centralized spot. It’s open source, so anyone can change the underlying code, and they can see what’s going on, being a truly peer-to-peer technology, or what is being called a “trust protocol”, once it doesn’t require powerful intermediaries to authenticate or to settle transactions, for this technology uses state-of-the-art cryptography. The other question that raises is once there’s a global, distributed database that can record the fact that someone has performed a specific transaction, what else could it record? The straight answer is that it could record any structured information, not just who paid whom but also who married whom, or who owns what and so on. In the case of the Internet of Things, there will be the need a Blockchain-settlement system underneath, or banks and other financial institutions won’t be able to settle trillions of real-time transactions between connected devices, as it is projected. Simply put, Blockchain is an immutable, unhackable distributed database of digital assets, a platform for truth and it’s a platform for trust, and the implications are quite staggering virtually across every industry and every aspect of our modern society. To simplify the way Blockchain works, it’s possible to enlist 4 main principles to this amazing underlying technology:

- Decentralized database: as mentioned before, the entire database and its complete history is fully available to everyone accessing Blockchain. There isn’t a specific party that controls the data or the information in it and every party is able to see and access the records of its transaction partners directly, without the need of an intermediary institution or party.

- Transparency and privacy:anyone with access to the Blockchain system is able to visualize every transaction record and its associated value in it. Users have a unique alphanumeric address composed by more that 30 character, which identify them and their transaction records, but users have the option of remaining anonymous or provide proof of their identity to others, for every transaction happens between Blockchain addresses.

- Computational logic: Given its digital nature, Blockchain transactions can be tied to computational logic and programmed, which means that its users are able to set up their own algorithms and transactional rules that automatically trigger transactions between them.

- Permanent and unchangeable rRecords: every transaction record that is entered the Blockchain database cannot be altered, because it’s directly linked to every transaction record that came before (reason why it contains the term “chain”). There are large amounts of algorithms and approaches deployed to secure all recordings on the database are permanent, chronologically ordered, and available to all users that are working on the network.

Blockchain can create a world in which contracts are embedded in digital code and stored in transparent, shared databases, where they are protected from deletion, tampering, hacking and revision. In this world every agreement, every process, every task, and every payment would have a digital record and signature that could be identified, validated, stored, and shared. Intermediaries like lawyers, brokers, and bankers might no longer be necessary. The nature of this technology can impact many areas. A study made by Stadista shows the areas that are going to feel the greatest impact by Blockchain globally:

Although it is difficult to predict how an underlying technology will be properly applied to different industries, it’s possible to understand that there are dozens of potential applications for Blockchain in virtually every industry. Of course, most attention has focused on applications in financial services, but concepts, prototypes, and investments are emerging in every major industry. The chart below shows the percentage of Blockchain use cases that were deployed in 2016 that are not related to Bitcoin or other digital currencies:

For a better and practical perspective, it’s possible to mention some of the main current use cases and how Blockchain will behave across different industries based on ongoing projects and other projections that are being widely reported in the news and by vendors and companies themselves, and the amount of possibilities are close to infinite:

- Financial Services: The financial services industry is a pioneer in exploring the uses of Blockchain technology for cryptocurrency transactions. Bitcoin uses Blockchain as its underlying technology. This is the industry where the greatest interest surrounding Blockchain is being generated, with applications for both public and permissioned Blockchains being explored, and the main reason why is, in contrast to today’s transaction networks, distributed ledgers eliminate the need for central authorities to certify ownership and clear transactions, and imagining a world in which people and companies can perform transactions securely without banks, stock exchanges, or payment processors is a very different one. Among some of the different use cases where Blockchain could be applied in the financial market, it’s possible to mention securities trading, where the Blockchain could enable near-instantaneous settlement, which could simplify middle and back-office processes and reduce settlement risk significantly, reduce banks’ infrastructure costs attributable to cross-border payments, securities trading, and regulatory compliance and the use of Blockchain for settling and clearing trades in stock markets.

- Government and Public Sector: There are quite a few compelling applications for Blockchain within government, especially when it comes to inefficient record-keeping methods. A Blockchain-based program could reduce the corruption and fraud associated with a centralized registry under the control of government officials by substituting a distributed, transparent ledger. Some other possible use cases may include creating inviolable voting records, vehicle registries, fraud-proof government benefits disbursements, and digital identities for individuals, such as refugees, who lack government-issued identity documents.

- Healthcare: The healthcare industry is said to be one of the fastest and earliest adopters of Blockchain technology, mainly as a mean of securing and safe-keeping digital assets. Healthcare companies intend to use Blockchain to store health care records from simple medical bills and communications between doctors and patients to claims and disputes. The cryptographic security would enhance the security of such records, while the immutable, irrevocable nature of transactions is intended to make claims processing more efficient and simplify dispute resolution. In addition, a community of people, including hospitals, doctors, patients, and insurance companies, could be part of the overall Blockchain network, reducing fraud in healthcare payments and subscription.

- Legal Affairs: Blockchain technology is built to hold a large amount of data, including entire contracts and their history. The impact of “smart contracts”, which are protocols that facilitate or enforce contract performance using Blockchain, will have a significant impact for many different industries, once they dismiss the need of an intermediate entity, such as a legal firm, as payment will happen based on certain established rules. Besides that, smart contracts are executed electronically, which creates a powerful warranty by taking it out of the control of a single party.

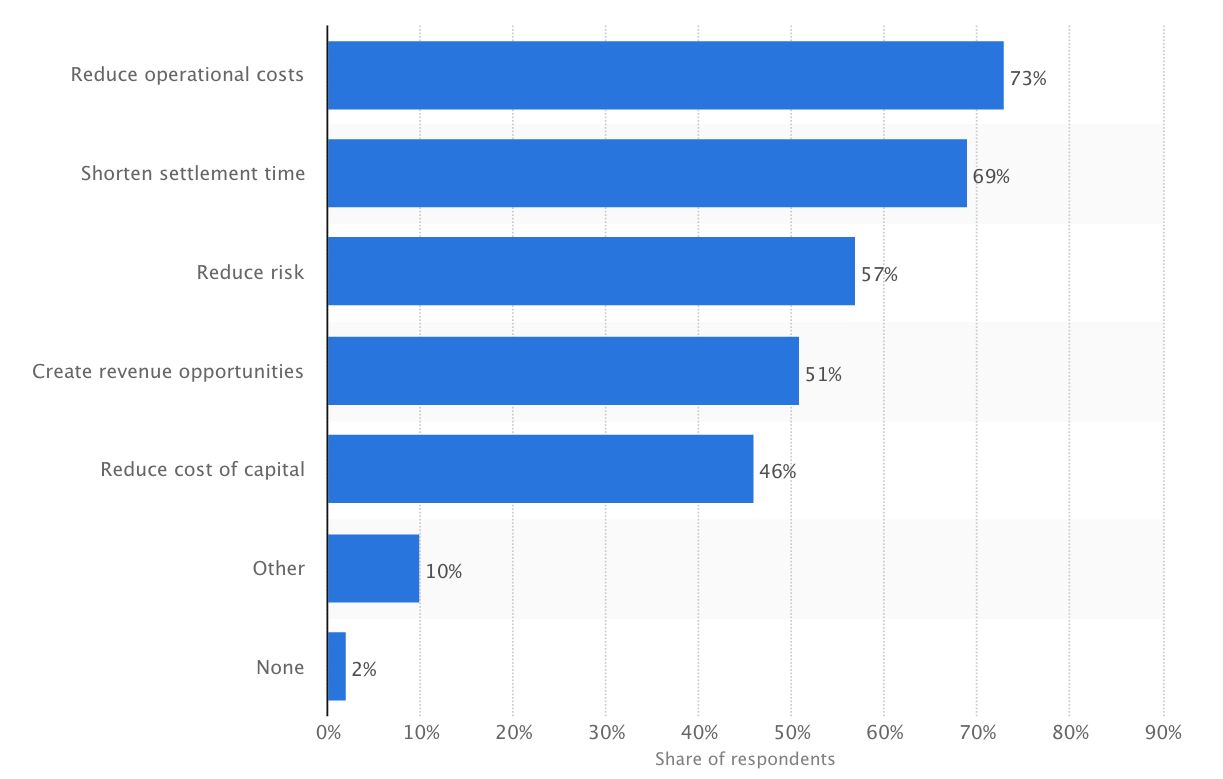

Blockchain counts on wide range of possibilities, with a unique and never seen potential to enhance the quality of service delivery and improving confidentiality, security and integrity of information. Benefits are numerous and may come within different perceptions from different industry segments. The chart below shows the leading benefits that companies globally expect from using Blockchain:

Perhaps, the greatest benefit that Blockchain offers is removing market friction. When the Internet appeared, it prepared to eliminate most of market’s friction, but since then, some frictions disappeared while others rose, such as frictions in information (such as inaccuracies or information risk), interaction (such as transactional costs or inaccessible marketplaces) and innovation (such as regulations or institutional inertia). As the market eliminates frictions, a new science of organization emerges, and industries and enterprises will take a very innovative new structure. Building these new structures with transparency, a strong foundation for trust and a cutting-edge technology, it can become the fastest path for further ecosystem evolution. Participants and assets once shut out of markets will be able join in, unleashing an accelerated flow of capital and unprecedented opportunities to create wealth around different economies and markets.

The possible applications that are powered by Blockchain technology are vast, and only time will tell what will work and be useful for the industry. Companies are just starting to sink their teeth into it. It’s true that Blockchain may be years away from widespread adoption, but the technology promises to have a significant effect on how many industries will plan and shape their businesses and implement their IT projects in the future.

This article was originally published on the IDG Network and can be accessed here.

Image source: Think Stock